66. Optimal Savings VI: EGM with JAX#

GPU

This lecture was built using a machine with access to a GPU — although it will also run without one.

Google Colab has a free tier with GPUs that you can access as follows:

Click on the “play” icon top right

Select Colab

Set the runtime environment to include a GPU

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install quantecon jax

66.1. Overview#

In this lecture, we’ll implement the endogenous grid method (EGM) using JAX.

This lecture builds on Optimal Savings V: The Endogenous Grid Method, which introduced EGM using NumPy.

By converting to JAX, we can leverage fast linear algebra, hardware accelerators, and JIT compilation for improved performance.

We’ll also use JAX’s vmap function to fully vectorize the Coleman-Reffett operator.

Let’s start with some standard imports:

import matplotlib.pyplot as plt

import jax

import jax.numpy as jnp

import quantecon as qe

from typing import NamedTuple

66.2. Implementation#

For details on the savings problem and the endogenous grid method (EGM), please see Optimal Savings V: The Endogenous Grid Method.

Here we focus on the JAX implementation of EGM.

We use the same setting as in Optimal Savings V: The Endogenous Grid Method:

\(u(c) = \ln c\),

production is Cobb-Douglas, and

the shocks are lognormal.

Here are the analytical solutions for comparison.

def v_star(x, α, β, μ):

"""

True value function

"""

c1 = jnp.log(1 - α * β) / (1 - β)

c2 = (μ + α * jnp.log(α * β)) / (1 - α)

c3 = 1 / (1 - β)

c4 = 1 / (1 - α * β)

return c1 + c2 * (c3 - c4) + c4 * jnp.log(x)

def σ_star(x, α, β):

"""

True optimal policy

"""

return (1 - α * β) * x

The Model class stores only the data (grids, shocks, and parameters).

Utility and production functions will be defined globally to work with JAX’s JIT compiler.

class Model(NamedTuple):

β: float # discount factor

μ: float # shock location parameter

s: float # shock scale parameter

s_grid: jnp.ndarray # exogenous savings grid

shocks: jnp.ndarray # shock draws

α: float # production function parameter

def create_model(

β: float = 0.96,

μ: float = 0.0,

s: float = 0.1,

grid_max: float = 4.0,

grid_size: int = 120,

shock_size: int = 250,

seed: int = 1234,

α: float = 0.4

) -> Model:

"""

Creates an instance of the optimal savings model.

"""

# Set up exogenous savings grid

s_grid = jnp.linspace(1e-4, grid_max, grid_size)

# Store shocks (with a seed, so results are reproducible)

key = jax.random.PRNGKey(seed)

shocks = jnp.exp(μ + s * jax.random.normal(key, shape=(shock_size,)))

return Model(β, μ, s, s_grid, shocks, α)

We define utility and production functions globally.

# Define utility and production functions with derivatives

u = lambda c: jnp.log(c)

u_prime = lambda c: 1 / c

u_prime_inv = lambda x: 1 / x

f = lambda k, α: k**α

f_prime = lambda k, α: α * k**(α - 1)

Here’s the Coleman-Reffett operator using EGM.

The key JAX feature here is vmap, which vectorizes the computation over the grid points.

def K(

c_in: jnp.ndarray, # Consumption values on the endogenous grid

x_in: jnp.ndarray, # Current endogenous grid

model: Model # Model specification

):

"""

The Coleman-Reffett operator using EGM

"""

β, μ, s, s_grid, shocks, α = model

σ = lambda x_val: jnp.interp(x_val, x_in, c_in)

# Define function to compute consumption at a single grid point

def compute_c(s):

# Approximate marginal utility ∫ u'(σ(f(s, α)z)) f'(s, α) z ϕ(z)dz

vals = u_prime(σ(f(s, α) * shocks)) * f_prime(s, α) * shocks

mu = jnp.mean(vals)

# Calculate consumption

return u_prime_inv(β * mu)

# Vectorize and calculate on all exogenous grid points

compute_c_vectorized = jax.vmap(compute_c)

c_out = compute_c_vectorized(s_grid)

# Determine corresponding endogenous grid

x_out = s_grid + c_out # x_i = s_i + c_i

return c_out, x_out

Now we create a model instance.

model = create_model()

s_grid = model.s_grid

The solver uses JAX’s jax.lax.while_loop for the iteration and is JIT-compiled for speed.

@jax.jit

def solve_model_time_iter(

model: Model,

c_init: jnp.ndarray,

x_init: jnp.ndarray,

tol: float = 1e-5,

max_iter: int = 1000

):

"""

Solve the model using time iteration with EGM.

"""

def condition(loop_state):

i, c, x, error = loop_state

return (error > tol) & (i < max_iter)

def body(loop_state):

i, c, x, error = loop_state

c_new, x_new = K(c, x, model)

error = jnp.max(jnp.abs(c_new - c))

return i + 1, c_new, x_new, error

# Initialize loop state

initial_state = (0, c_init, x_init, tol + 1)

# Run the loop

i, c, x, error = jax.lax.while_loop(condition, body, initial_state)

return c, x

We solve the model starting from an initial guess.

c_init = jnp.copy(s_grid)

x_init = s_grid + c_init

c, x = solve_model_time_iter(model, c_init, x_init)

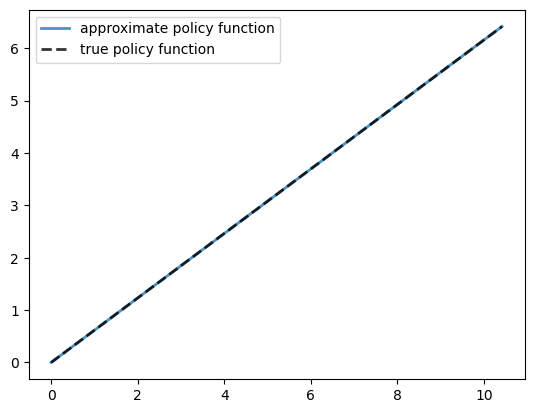

Let’s plot the resulting policy against the analytical solution.

fig, ax = plt.subplots()

ax.plot(x, c, lw=2,

alpha=0.8, label='approximate policy function')

ax.plot(x, σ_star(x, model.α, model.β), 'k--',

lw=2, alpha=0.8, label='true policy function')

ax.legend()

plt.show()

The fit is very good.

max_dev = jnp.max(jnp.abs(c - σ_star(x, model.α, model.β)))

print(f"Maximum absolute deviation: {max_dev:.7}")

Maximum absolute deviation: 1.430511e-06

The JAX implementation is very fast thanks to JIT compilation and vectorization.

with qe.Timer(precision=8):

c, x = solve_model_time_iter(model, c_init, x_init)

jax.block_until_ready(c)

0.00274968 seconds elapsed

This speed comes from:

JIT compilation of the entire solver

Vectorization via

vmapin the Coleman-Reffett operatorUse of

jax.lax.while_loopinstead of a Python loopEfficient JAX array operations throughout

66.3. Exercises#

Exercise 66.1

Solve the optimal savings problem with CRRA utility

Compare the optimal policies for values of \(\gamma\) approaching 1 from above (e.g., 1.05, 1.1, 1.2).

Show that as \(\gamma \to 1\), the optimal policy converges to the policy obtained with log utility (\(\gamma = 1\)).

Hint: Use values of \(\gamma\) close to 1 to ensure the endogenous grids have similar coverage and make visual comparison easier.

Solution

We need to create a version of the Coleman-Reffett operator and solver that work with CRRA utility.

The key is to parameterize the utility functions by \(\gamma\).

def u_crra(c, γ):

return (c**(1 - γ) - 1) / (1 - γ)

def u_prime_crra(c, γ):

return c**(-γ)

def u_prime_inv_crra(x, γ):

return x**(-1/γ)

Now we create a version of the Coleman-Reffett operator that takes \(\gamma\) as a parameter.

def K_crra(

c_in: jnp.ndarray, # Consumption values on the endogenous grid

x_in: jnp.ndarray, # Current endogenous grid

model: Model, # Model specification

γ: float # CRRA parameter

):

"""

The Coleman-Reffett operator using EGM with CRRA utility

"""

# Simplify names

β, α = model.β, model.α

s_grid, shocks = model.s_grid, model.shocks

# Linear interpolation of policy using endogenous grid

σ = lambda x_val: jnp.interp(x_val, x_in, c_in)

# Define function to compute consumption at a single grid point

def compute_c(s):

vals = u_prime_crra(σ(f(s, α) * shocks), γ) * f_prime(s, α) * shocks

return u_prime_inv_crra(β * jnp.mean(vals), γ)

# Vectorize over grid using vmap

compute_c_vectorized = jax.vmap(compute_c)

c_out = compute_c_vectorized(s_grid)

# Determine corresponding endogenous grid

x_out = s_grid + c_out # x_i = s_i + c_i

return c_out, x_out

We also need a solver that uses this operator.

@jax.jit

def solve_model_crra(model: Model,

c_init: jnp.ndarray,

x_init: jnp.ndarray,

γ: float,

tol: float = 1e-5,

max_iter: int = 1000):

"""

Solve the model using time iteration with EGM and CRRA utility.

"""

def condition(loop_state):

i, c, x, error = loop_state

return (error > tol) & (i < max_iter)

def body(loop_state):

i, c, x, error = loop_state

c_new, x_new = K_crra(c, x, model, γ)

error = jnp.max(jnp.abs(c_new - c))

return i + 1, c_new, x_new, error

# Initialize loop state

initial_state = (0, c_init, x_init, tol + 1)

# Run the loop

i, c, x, error = jax.lax.while_loop(condition, body, initial_state)

return c, x

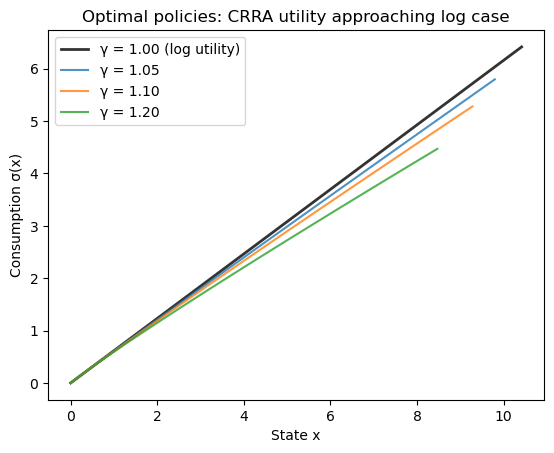

Now we solve for \(\gamma = 1\) (log utility) and values approaching 1 from above.

γ_values = [1.0, 1.05, 1.1, 1.2]

policies = {}

endogenous_grids = {}

model_crra = create_model()

for γ in γ_values:

c_init = jnp.copy(model_crra.s_grid)

x_init = model_crra.s_grid + c_init

c_gamma, x_gamma = solve_model_crra(model_crra, c_init, x_init, γ)

jax.block_until_ready(c_gamma)

policies[γ] = c_gamma

endogenous_grids[γ] = x_gamma

print(f"Solved for γ = {γ}")

Solved for γ = 1.0

Solved for γ = 1.05

Solved for γ = 1.1

Solved for γ = 1.2

Plot the policies on their endogenous grids.

fig, ax = plt.subplots()

for γ in γ_values:

x = endogenous_grids[γ]

if γ == 1.0:

ax.plot(x, policies[γ], 'k-', linewidth=2,

label=f'γ = {γ:.2f} (log utility)', alpha=0.8)

else:

ax.plot(x, policies[γ], label=f'γ = {γ:.2f}', alpha=0.8)

ax.set_xlabel('State x')

ax.set_ylabel('Consumption σ(x)')

ax.legend()

ax.set_title('Optimal policies: CRRA utility approaching log case')

plt.show()

Note that the plots for \(\gamma > 1\) do not cover the entire x-axis range shown.

This is because the endogenous grid \(x = s + \sigma(s)\) depends on the consumption policy, which varies with \(\gamma\).

Let’s check the maximum deviation between the log utility case (\(\gamma = 1.0\)) and values approaching from above.

for γ in [1.05, 1.1, 1.2]:

max_diff = jnp.max(jnp.abs(policies[1.0] - policies[γ]))

print(f"Max difference between γ=1.0 and γ={γ}: {max_diff:.6}")

Max difference between γ=1.0 and γ=1.05: 0.619199

Max difference between γ=1.0 and γ=1.1: 1.1362

Max difference between γ=1.0 and γ=1.2: 1.94592

As expected, the differences decrease as \(\gamma\) approaches 1 from above, confirming convergence.