9. Some Probability Distributions#

This lecture is a supplement to this lecture on statistics with matrices.

It describes some popular distributions and uses Python to sample from them.

It also describes a way to sample from an arbitrary probability distribution that you make up by transforming a sample from a uniform probability distribution.

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install prettytable

As usual, we’ll start with some imports

import numpy as np

import matplotlib.pyplot as plt

import prettytable as pt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib_inline.backend_inline import set_matplotlib_formats

set_matplotlib_formats('retina')

9.1. Some Discrete Probability Distributions#

Let’s write some Python code to compute means and variances of some univariate random variables.

We’ll use our code to

compute population means and variances from the probability distribution

generate a sample of \(N\) independently and identically distributed draws and compute sample means and variances

compare population and sample means and variances

9.2. Geometric distribution#

A discrete geometric distribution has probability mass function

where \(k = 1, 2, \ldots\) is the number of trials before the first success.

The mean and variance of this one-parameter probability distribution are

Let’s use Python draw observations from the distribution and compare the sample mean and variance with the theoretical results.

rng = np.random.default_rng()

# specify parameters

p, n = 0.3, 1_000_000

# draw observations from the distribution

x = rng.geometric(p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

# compare with theoretical results

print("\nThe population mean is: ", 1/p)

print("The population variance is: ", (1-p)/(p**2))

The sample mean is: 3.340194

The sample variance is: 7.826038042363999

The population mean is: 3.3333333333333335

The population variance is: 7.777777777777778

9.3. Pascal (negative binomial) distribution#

Consider a sequence of independent Bernoulli trials.

Let \(p\) be the probability of success.

Let \(X\) be a random variable that represents the number of failures before we get \(r\) successes.

Its distribution is

Here, we choose from among \(k+r-1\) possible outcomes because the last draw is by definition a success.

We compute the mean and variance to be

# specify parameters

r, p, n = 10, 0.3, 1_000_000

# draw observations from the distribution

x = rng.negative_binomial(r, p, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", r*(1-p)/p)

print("The population variance is: ", r*(1-p)/p**2)

The sample mean is: 23.313391

The sample variance is: 77.433113081119

The population mean is: 23.333333333333336

The population variance is: 77.77777777777779

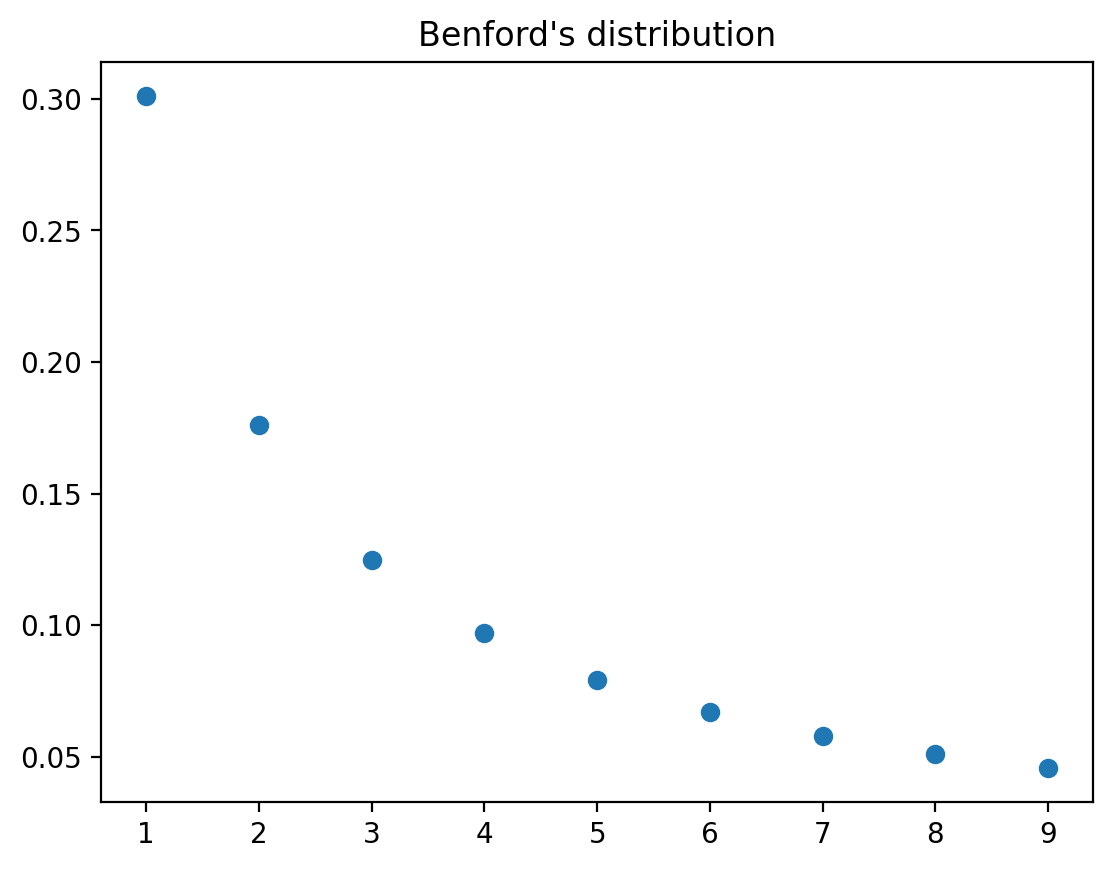

9.4. Newcomb–Benford distribution#

The Newcomb–Benford law fits many data sets, e.g., reports of incomes to tax authorities, in which the leading digit is more likely to be small than large.

See https://en.wikipedia.org/wiki/Benford’s_law

A Benford probability distribution is

where \(d\in\{1,2,\cdots,9\}\) can be thought of as a first digit in a sequence of digits.

This is a well defined discrete distribution since we can verify that probabilities are nonnegative and sum to \(1\).

The mean and variance of a Benford distribution are

We verify the above and compute the mean and variance using numpy.

Benford_pmf = np.array([np.log10(1+1/d) for d in range(1,10)])

k = np.arange(1, 10)

# mean

mean = k @ Benford_pmf

# variance

var = ((k - mean) ** 2) @ Benford_pmf

# verify sum to 1

print(np.sum(Benford_pmf))

print(mean)

print(var)

0.9999999999999999

3.4402369671232065

6.056512631375667

# plot distribution

plt.plot(range(1,10), Benford_pmf, 'o')

plt.title('Benford\'s distribution')

plt.show()

Now let’s turn to some continuous random variables.

9.5. Univariate Gaussian distribution#

We write

to indicate the probability distribution

In the below example, we set \(\mu = 0, \sigma = 0.1\).

# specify parameters

μ, σ = 0, 0.1

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = rng.normal(μ, σ, n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ_hat = np.std(x)

print("The sample mean is: ", μ_hat)

print("The sample standard deviation is: ", σ_hat)

The sample mean is: -8.746457562470357e-05

The sample standard deviation is: 0.10006903517555081

# compare

print(μ-μ_hat < 1e-3)

print(σ-σ_hat < 1e-3)

True

True

9.6. Uniform Distribution#

The population mean and variance are

# specify parameters

a, b = 10, 20

# specify number of draws

n = 1_000_000

# draw observations from the distribution

x = a + (b-a)*rng.random(n)

# compute sample mean and variance

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

print("\nThe population mean is: ", (a+b)/2)

print("The population variance is: ", (b-a)**2/12)

The sample mean is: 15.00243694446103

The sample variance is: 8.316698298098494

The population mean is: 15.0

The population variance is: 8.333333333333334

9.7. A Mixed Discrete-Continuous Distribution#

We’ll motivate this example with a little story.

Suppose that to apply for a job you take an interview and either pass or fail it.

You have \(5\%\) chance to pass an interview and you know your salary will uniformly distributed in the interval 300~400 a day only if you pass.

We can describe your daily salary as a discrete-continuous variable with the following probabilities:

Let’s start by generating a random sample and computing sample moments.

x = rng.random(1_000_000)

# x[x > 0.95] = 100*x[x > 0.95]+300

x[x > 0.95] = 100*rng.random(len(x[x > 0.95]))+300

x[x <= 0.95] = 0

μ_hat = np.mean(x)

σ2_hat = np.var(x)

print("The sample mean is: ", μ_hat, "\nThe sample variance is: ", σ2_hat)

The sample mean is: 17.443243551033635

The sample variance is: 5841.191856127901

The analytical mean and variance can be computed:

mean = 0.0005*0.5*(400**2 - 300**2)

var = 0.95*17.5**2+0.0005/3*((400-17.5)**3-(300-17.5)**3)

print("mean: ", mean)

print("variance: ", var)

mean: 17.5

variance: 5860.416666666666

9.8. Drawing a Random Number from a Particular Distribution#

Suppose we have at our disposal a pseudo random number that draws a uniform random variable, i.e., one with probability distribution

How can we transform \(\tilde{X}\) to get a random variable \(X\) for which \(\textrm{Prob}\{X=i\}=f_i,\quad i=0,\ldots,I-1\), where \(f_i\) is an arbitary discrete probability distribution on \(i=0,1,\dots,I-1\)?

The key tool is the inverse of a cumulative distribution function (CDF).

Observe that the CDF of a distribution is monotone and non-decreasing, taking values between \(0\) and \(1\).

We can draw a sample of a random variable \(X\) with a known CDF as follows:

draw a random variable \(u\) from a uniform distribution on \([0,1]\)

pass the sample value of \(u\) into the “inverse” target CDF for \(X\)

\(X\) has the target CDF

Thus, knowing the “inverse” CDF of a distribution is enough to simulate from this distribution.

Note

The “inverse” CDF needs to exist for this method to work.

The inverse CDF is

Here we use infimum because a CDF is a non-decreasing and right-continuous function.

Thus, suppose that

\(U\) is a uniform random variable \(U\in[0,1]\)

We want to sample a random variable \(X\) whose CDF is \(F\).

It turns out that if we use draw uniform random numbers \(U\) and then compute \(X\) from

then \(X\) is a random variable with CDF \(F_X(x)=F(x)=\textrm{Prob}\{X\le x\}\).

We’ll verify this in the special case in which \(F\) is continuous and bijective so that its inverse function exists and can be denoted by \(F^{-1}\).

Note that

where the last equality occurs because \(U\) is distributed uniformly on \([0,1]\) while \(F(x)\) is a constant given \(x\) that also lies on \([0,1]\).

Let’s use numpy to compute some examples.

Example: A continuous geometric (exponential) distribution

Let \(X\) follow a geometric distribution, with parameter \(\lambda>0\).

Its density function is

Its CDF is

Let \(U\) follow a uniform distribution on \([0,1]\).

\(X\) is a random variable such that \(U=F(X)\).

The distribution \(X\) can be deduced from

Let’s draw \(u\) from \(U[0,1]\) and calculate \(x=\frac{log(1-U)}{-\lambda}\).

We’ll check whether \(X\) seems to follow a continuous geometric (exponential) distribution.

Let’s check with numpy.

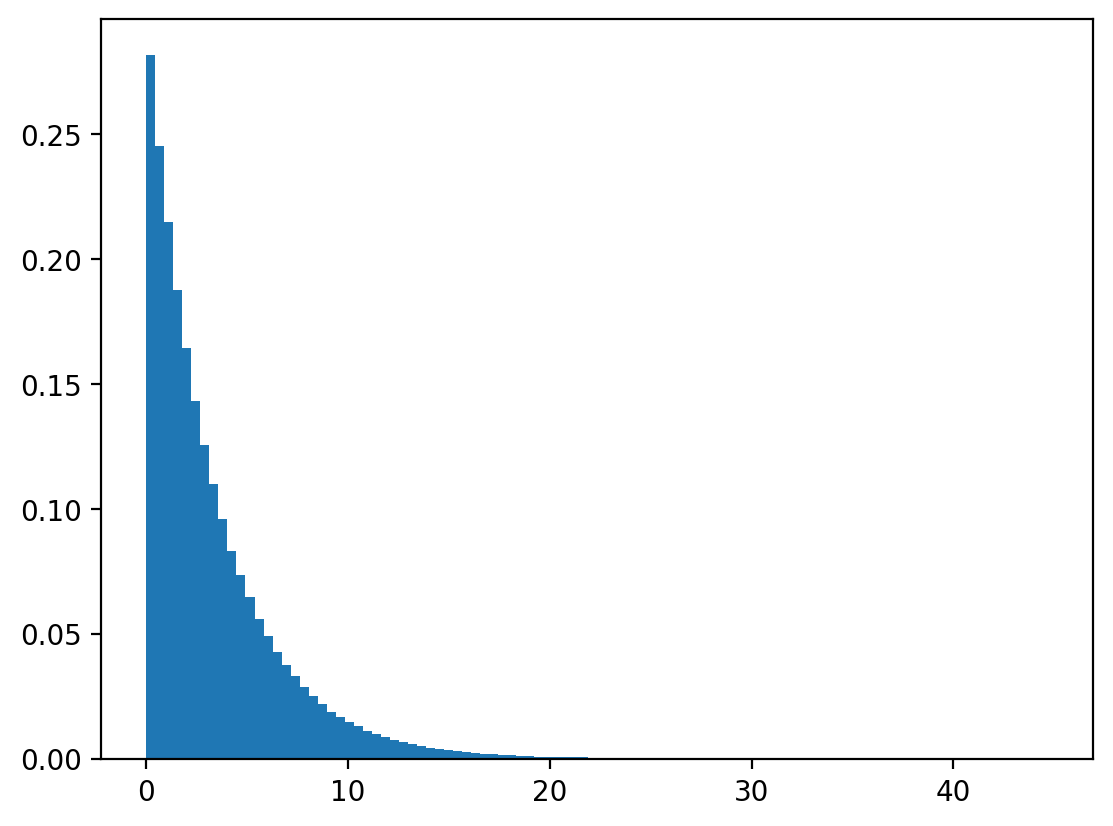

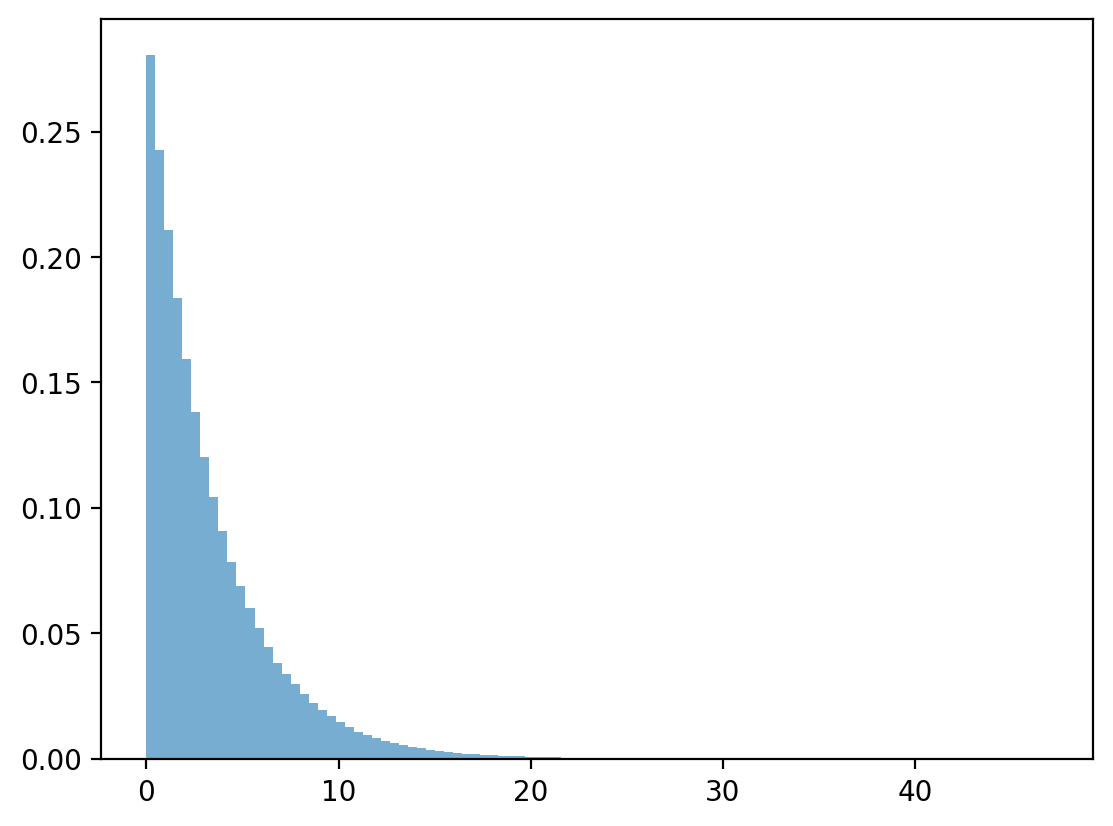

n, λ = 1_000_000, 0.3

# draw uniform numbers

u = rng.random(n)

# transform

x = -np.log(1-u)/λ

# draw geometric distributions

x_g = rng.exponential(1 / λ, n)

# plot and compare

plt.hist(x, bins=100, density=True)

plt.show()

plt.hist(x_g, bins=100, density=True, alpha=0.6)

plt.show()

Geometric distribution

Let \(X\) distributed geometrically, that is

Its CDF is given by

Again, let \(\tilde{U}\) follow a uniform distribution and we want to find \(X\) such that \(F(X)=\tilde{U}\).

Let’s deduce the distribution of \(X\) from

However, \(\tilde{U}=F^{-1}(X)\) may not be an integer for any \(x\geq0\).

So let

where \(\lceil . \rceil\) is the ceiling function.

Thus \(x\) is the smallest integer such that the discrete geometric CDF is greater than or equal to \(\tilde{U}\).

We can verify that \(x\) is indeed geometrically distributed by the following numpy program.

Note

The exponential distribution is the continuous analog of geometric distribution.

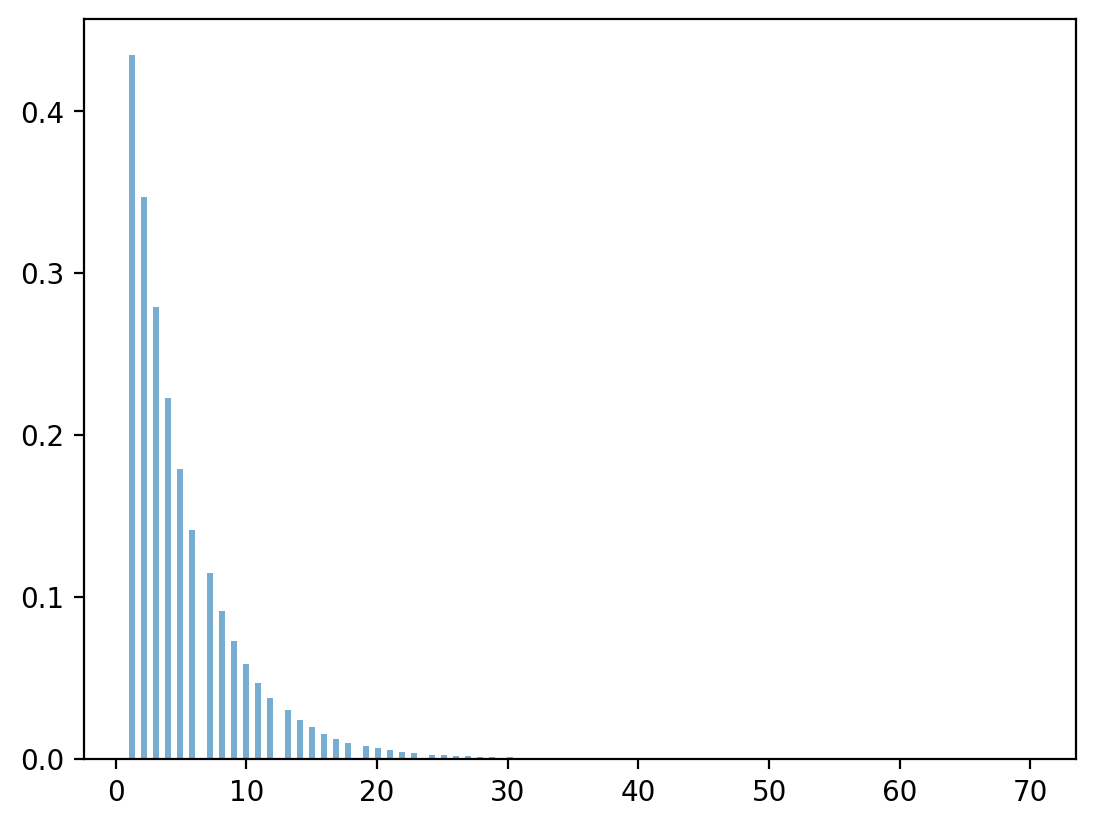

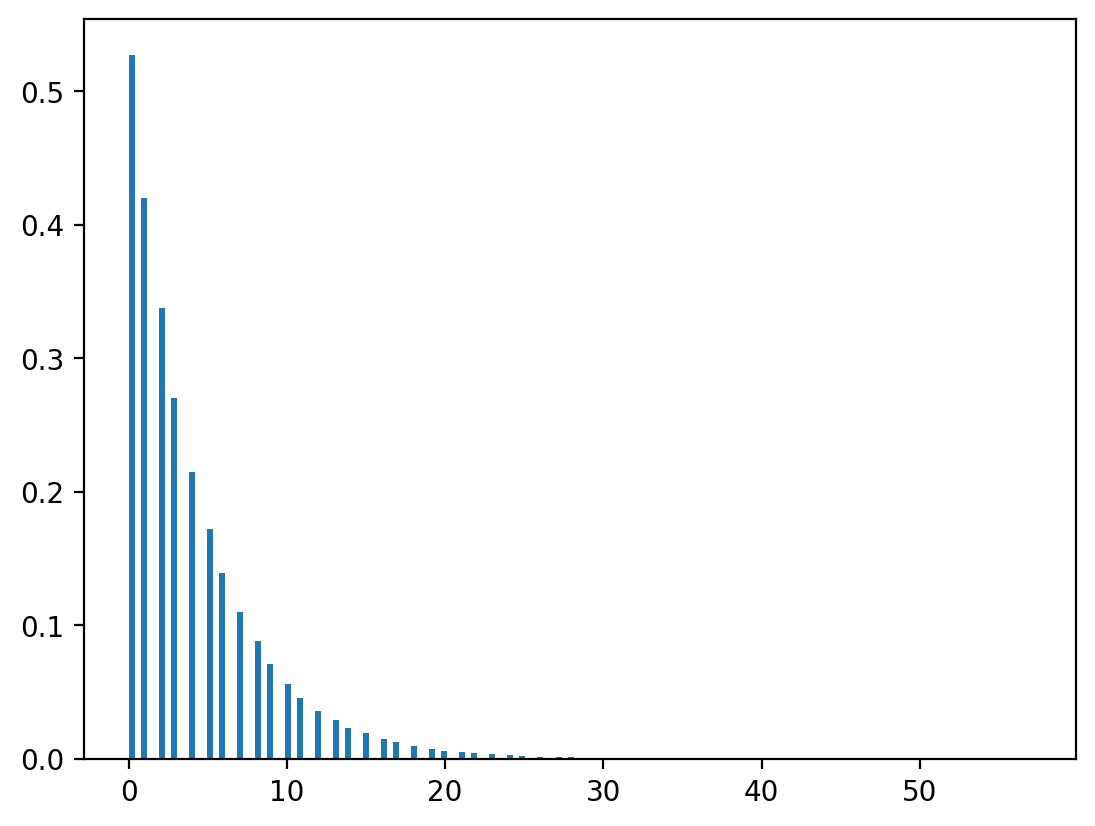

n, λ = 1_000_000, 0.8

# draw uniform numbers

u = rng.random(n)

# transform

x = np.ceil(np.log(1-u)/np.log(λ) - 1)

# draw geometric distributions

x_g = rng.geometric(1-λ, n)

# plot and compare

plt.hist(x, bins=150, density=True)

plt.show()

rng.geometric(1-λ, n).max()

np.int64(64)

np.log(0.4)/np.log(0.3)

np.float64(0.7610560044063083)

plt.hist(x_g, bins=150, density=True, alpha=0.6)

plt.show()