65. Optimal Savings V: The Endogenous Grid Method#

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install quantecon

65.1. Overview#

Previously, we solved the optimal savings problem using

We found time iteration to be significantly more accurate and efficient.

In this lecture, we’ll look at a clever twist on time iteration called the endogenous grid method (EGM).

EGM is a numerical method for implementing policy iteration invented by Chris Carroll.

The original reference is [Carroll, 2006].

For now we will focus on a clean and simple implementation of EGM that stays close to the underlying mathematics.

Then, in Optimal Savings VI: EGM with JAX, we will construct a fully vectorized and parallelized version of EGM based on JAX.

Let’s start with some standard imports:

import matplotlib.pyplot as plt

import numpy as np

import quantecon as qe

65.2. Key Idea#

First we remind ourselves of the theory and then we turn to numerical methods.

65.2.1. Theory#

We work with the model set out in Optimal Savings IV: Time Iteration, following the same terminology and notation.

As we saw, the Coleman-Reffett operator is a nonlinear operator \(K\) engineered so that the optimal policy \(\sigma^*\) is a fixed point of \(K\).

It takes as its argument a continuous strictly increasing consumption policy \(\sigma \in \Sigma\).

It returns a new function \(K \sigma\), where \((K \sigma)(x)\) is the \(c \in (0, \infty)\) that solves

65.2.2. Exogenous Grid#

As discussed in Optimal Savings IV: Time Iteration, to implement the method on a computer, we represent a policy function by a set of values on a finite grid.

The function itself is reconstructed from this representation when necessary, using interpolation or some other method.

Our previous strategy in Optimal Savings IV: Time Iteration for obtaining a finite representation of an updated consumption policy was to

fix a grid of income points \(\{x_i\}\)

calculate the consumption value \(c_i\) corresponding to each \(x_i\) using (65.1) and a root-finding routine

Each \(c_i\) is then interpreted as the value of the function \(K \sigma\) at \(x_i\).

Thus, with the pairs \(\{(x_i, c_i)\}\) in hand, we can reconstruct \(K \sigma\) via approximation.

Iteration then continues…

65.2.3. Endogenous Grid#

The method discussed above requires a root-finding routine to find the \(c_i\) corresponding to a given income value \(x_i\).

Root-finding is costly because it typically involves a significant number of function evaluations.

As pointed out by Carroll [Carroll, 2006], we can avoid this step if \(x_i\) is chosen endogenously.

The only assumption required is that \(u'\) is invertible on \((0, \infty)\).

Let \((u')^{-1}\) be the inverse function of \(u'\).

The idea is this:

First, we fix an exogenous grid \(\{s_i\}\) for savings (\(s = x - c\)).

Then we obtain \(c_i\) via

Finally, for each \(c_i\) we set \(x_i = c_i + s_i\).

Importantly, each \((x_i, c_i)\) pair constructed in this manner satisfies (65.1).

With the points \(\{x_i, c_i\}\) in hand, we can reconstruct \(K \sigma\) via approximation as before.

The name EGM comes from the fact that the grid \(\{x_i\}\) is determined endogenously.

65.3. Implementation#

As in Optimal Savings IV: Time Iteration, we will start with a simple setting where

\(u(c) = \ln c\),

the function \(f\) has a Cobb-Douglas specification, and

the shocks are lognormal.

This will allow us to make comparisons with the analytical solutions.

def v_star(x, α, β, μ):

"""

True value function

"""

c1 = np.log(1 - α * β) / (1 - β)

c2 = (μ + α * np.log(α * β)) / (1 - α)

c3 = 1 / (1 - β)

c4 = 1 / (1 - α * β)

return c1 + c2 * (c3 - c4) + c4 * np.log(x)

def σ_star(x, α, β):

"""

True optimal policy

"""

return (1 - α * β) * x

We reuse the Model structure from Optimal Savings IV: Time Iteration.

from typing import NamedTuple, Callable

class Model(NamedTuple):

u: Callable # utility function

f: Callable # production function

β: float # discount factor

μ: float # shock location parameter

ν: float # shock scale parameter

s_grid: np.ndarray # exogenous savings grid

shocks: np.ndarray # shock draws

α: float # production function parameter

u_prime: Callable # derivative of utility

f_prime: Callable # derivative of production

u_prime_inv: Callable # inverse of u_prime

def create_model(

u: Callable,

f: Callable,

β: float = 0.96,

μ: float = 0.0,

ν: float = 0.1,

grid_max: float = 4.0,

grid_size: int = 120,

shock_size: int = 250,

seed: int = 1234,

α: float = 0.4,

u_prime: Callable = None,

f_prime: Callable = None,

u_prime_inv: Callable = None

) -> Model:

"""

Creates an instance of the optimal savings model.

"""

# Set up exogenous savings grid

s_grid = np.linspace(1e-4, grid_max, grid_size)

# Store shocks (with a seed, so results are reproducible)

np.random.seed(seed)

shocks = np.exp(μ + ν * np.random.randn(shock_size))

return Model(

u, f, β, μ, ν, s_grid, shocks, α, u_prime, f_prime, u_prime_inv

)

65.3.1. The Operator#

Here’s an implementation of \(K\) using EGM as described above.

def K(

c_in: np.ndarray, # Consumption values on the endogenous grid

x_in: np.ndarray, # Current endogenous grid

model: Model # Model specification

):

"""

An implementation of the Coleman-Reffett operator using EGM.

"""

# Simplify names

u, f, β, μ, ν, s_grid, shocks, α, u_prime, f_prime, u_prime_inv = model

# Linear interpolation of policy on the endogenous grid

σ = lambda x: np.interp(x, x_in, c_in)

# Allocate memory for new consumption array

c_out = np.empty_like(s_grid)

for i, s in enumerate(s_grid):

# Approximate marginal utility ∫ u'(σ(f(s, α)z)) f'(s, α) z ϕ(z)dz

vals = u_prime(σ(f(s, α) * shocks)) * f_prime(s, α) * shocks

mu = np.mean(vals)

# Compute consumption

c_out[i] = u_prime_inv(β * mu)

# Determine corresponding endogenous grid

x_out = s_grid + c_out # x_i = s_i + c_i

return c_out, x_out

Note the lack of any root-finding algorithm.

Note

The routine is still not particularly fast because we are using pure Python loops.

But in the next lecture (Optimal Savings VI: EGM with JAX) we will use a fully vectorized and efficient solution.

65.3.2. Testing#

First we create an instance.

# Define utility and production functions with derivatives

u = lambda c: np.log(c)

u_prime = lambda c: 1 / c

u_prime_inv = lambda x: 1 / x

f = lambda k, α: k**α

f_prime = lambda k, α: α * k**(α - 1)

model = create_model(u=u, f=f, u_prime=u_prime,

f_prime=f_prime, u_prime_inv=u_prime_inv)

s_grid = model.s_grid

Here’s our solver routine:

def solve_model_time_iter(

model: Model, # Model details

c_init: np.ndarray, # initial guess of consumption on EG

x_init: np.ndarray, # initial guess of endogenous grid

tol: float = 1e-5, # Error tolerance

max_iter: int = 1000, # Max number of iterations of K

verbose: bool = True # If true print output

):

"""

Solve the model using time iteration with EGM.

"""

c, x = c_init, x_init

error = tol + 1

i = 0

while error > tol and i < max_iter:

c_new, x_new = K(c, x, model)

error = np.max(np.abs(c_new - c))

c, x = c_new, x_new

i += 1

if verbose:

print(f"Iteration {i}, error = {error}")

if i == max_iter:

print("Warning: maximum iterations reached")

return c, x

Let’s call it:

c_init = np.copy(s_grid)

x_init = s_grid + c_init

c, x = solve_model_time_iter(model, c_init, x_init)

Iteration 1, error = 1.208333333333333

Iteration 2, error = 0.6834464555052788

Iteration 3, error = 0.3126351338414741

Iteration 4, error = 0.12905177785629984

Iteration 5, error = 0.05099394329538409

Iteration 6, error = 0.01980055511172729

Iteration 7, error = 0.007636088144566955

Iteration 8, error = 0.002937098891578671

Iteration 9, error = 0.0011285611196765188

Iteration 10, error = 0.00043347299641638415

Iteration 11, error = 0.00016646919532892213

Iteration 12, error = 6.392646634978405e-05

Iteration 13, error = 2.4548101555943447e-05

Iteration 14, error = 9.426520908739633e-06

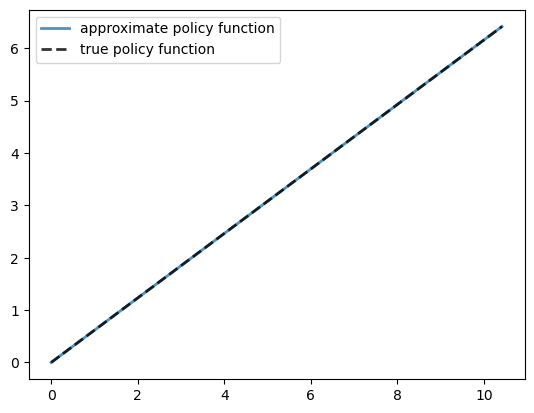

Here is a plot of the resulting policy, compared with the true policy:

fig, ax = plt.subplots()

ax.plot(x, c, lw=2,

alpha=0.8, label='approximate policy function')

ax.plot(x, σ_star(x, model.α, model.β), 'k--',

lw=2, alpha=0.8, label='true policy function')

ax.legend()

plt.show()

The maximal absolute deviation between the two policies is

np.max(np.abs(c - σ_star(x, model.α, model.β)))

np.float64(2.2564941266622895e-06)

Here’s the execution time:

with qe.Timer():

c, x = solve_model_time_iter(model, c_init, x_init, verbose=False)

0.0302 seconds elapsed

EGM is faster than time iteration because it avoids numerical root-finding.

Instead, we invert the marginal utility function directly, which is much more efficient.

In Optimal Savings VI: EGM with JAX, we will use a fully vectorized and efficient version of EGM that is also parallelized using JAX.

This provides an extremely fast way to solve the optimal consumption problem we have been studying for the last few lectures.