57. Job Search VIII: Search with Learning#

In addition to what’s in Anaconda, this lecture deploys the libraries:

!pip install interpolation

57.1. Overview#

In this lecture, we consider an extension of the previously studied job search model of McCall [McCall, 1970].

We’ll build on a model of Bayesian learning discussed in this lecture on the topic of exchangeability and its relationship to the concept of IID (identically and independently distributed) random variables and to Bayesian updating.

In the McCall model, an unemployed worker decides when to accept a permanent job at a specific fixed wage, given

his or her discount factor

the level of unemployment compensation

the distribution from which wage offers are drawn

In the version considered below, the wage distribution is unknown and must be learned.

The following is based on the presentation in [Ljungqvist and Sargent, 2018], section 6.6.

Let’s start with some imports

import matplotlib.pyplot as plt

from numba import jit, prange, vectorize

from interpolation import mlinterp

from math import gamma

import numpy as np

from matplotlib import cm

import scipy.optimize as op

from scipy.stats import cumfreq, beta

57.1.1. Model Features#

Infinite horizon dynamic programming with two states and one binary control.

Bayesian updating to learn the unknown distribution.

57.2. Model#

Let’s first review the basic McCall model [McCall, 1970] and then add the variation we want to consider.

57.2.1. The Basic McCall Model#

Recall that, in the baseline model, an unemployed worker is presented in each period with a permanent job offer at wage \(W_t\).

At time \(t\), our worker either

accepts the offer and works permanently at constant wage \(W_t\)

rejects the offer, receives unemployment compensation \(c\) and reconsiders next period

The wage sequence \({W_t}\) is IID and generated from known density \(q\).

The worker aims to maximize the expected discounted sum of earnings \(\mathbb{E} \sum_{t=0}^{\infty}\beta^t y_t\).

Let \(v(w)\) be the optimal value of the problem for a previously unemployed worker who has just received offer \(w\) and is yet to decide whether to accept or reject the offer.

The value function \(v\) satisfies the recursion

The optimal policy has the form \(\mathbf{1}\{w \geq \bar w\}\), where \(\bar w\) is a constant called the reservation wage.

57.2.2. Offer Distribution Unknown#

Now let’s extend the model by considering the variation presented in [Ljungqvist and Sargent, 2018], section 6.6.

The model is as above, apart from the fact that

the density \(q\) is unknown

the worker learns about \(q\) by starting with a prior and updating based on wage offers that he/she observes

The worker knows there are two possible distributions \(F\) and \(G\).

These two distributions have densities \(f\) and \(g\), repectively.

Just before time starts, “nature” selects \(q\) to be either \(f\) or \(g\).

This is then the wage distribution from which the entire sequence \({W_t}\) will be drawn.

The worker does not know which distribution nature has drawn, but the worker does know the two possible distributions \(f\) and \(g\).

The worker puts a (subjective) prior probability \(\pi_0\) on \(f\) having been chosen.

The worker’s time \(0\) subjective distribution for the distribution of \(W_0\) is

The worker’s time \(t\) subjective belief about the the distribution of \(W_t\) is

where \(\pi_t\) updates via

This last expression follows from Bayes’ rule, which tells us that

and

The fact that (57.2) is recursive allows us to progress to a recursive solution method.

Letting

and

we can express the value function for the unemployed worker recursively as follows

Notice that the current guess \(\pi\) is a state variable, since it affects the worker’s perception of probabilities for future rewards.

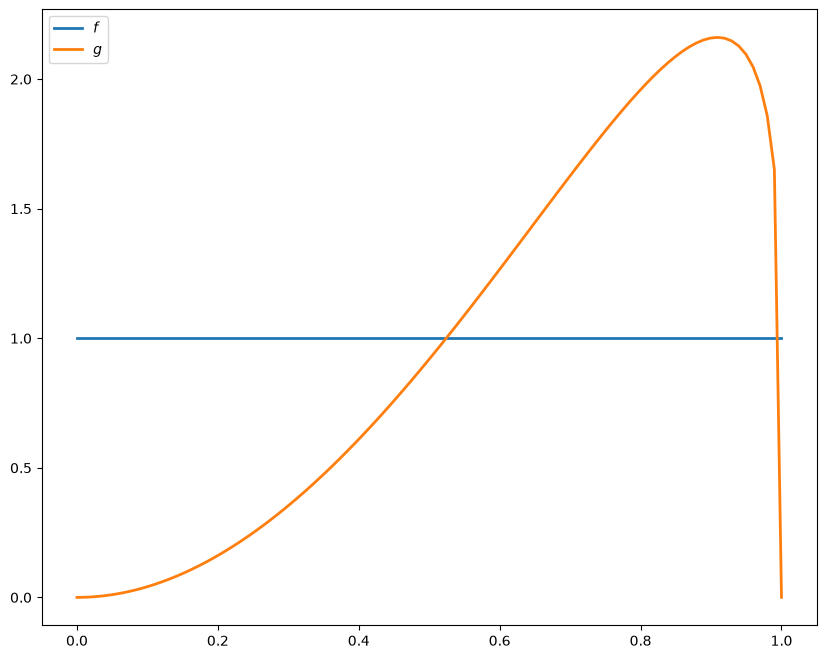

57.2.3. Parameterization#

Following section 6.6 of [Ljungqvist and Sargent, 2018], our baseline parameterization will be

\(f\) is \(\operatorname{Beta}(1, 1)\)

\(g\) is \(\operatorname{Beta}(3, 1.2)\)

\(\beta = 0.95\) and \(c = 0.3\)

The densities \(f\) and \(g\) have the following shape

@vectorize

def p(x, a, b):

r = gamma(a + b) / (gamma(a) * gamma(b))

return r * x**(a-1) * (1 - x)**(b-1)

x_grid = np.linspace(0, 1, 100)

f = lambda x: p(x, 1, 1)

g = lambda x: p(x, 3, 1.2)

fig, ax = plt.subplots(figsize=(10, 8))

ax.plot(x_grid, f(x_grid), label='$f$', lw=2)

ax.plot(x_grid, g(x_grid), label='$g$', lw=2)

ax.legend()

plt.show()

57.2.4. Looking Forward#

What kind of optimal policy might result from (57.3) and the parameterization specified above?

Intuitively, if we accept at \(w_a\) and \(w_a\leq w_b\), then – all other things being given – we should also accept at \(w_b\).

This suggests a policy of accepting whenever \(w\) exceeds some threshold value \(\bar w\).

But \(\bar w\) should depend on \(\pi\) – in fact, it should be decreasing in \(\pi\) because

\(f\) is a less attractive offer distribution than \(g\)

larger \(\pi\) means more weight on \(f\) and less on \(g\)

Thus, larger \(\pi\) depresses the worker’s assessment of her future prospects, so relatively low current offers become more attractive.

Summary: We conjecture that the optimal policy is of the form \(\mathbb 1{w\geq \bar w(\pi) }\) for some decreasing function \(\bar w\).

57.3. Take 1: Solution by VFI#

Let’s set about solving the model and see how our results match with our intuition.

We begin by solving via value function iteration (VFI), which is natural but ultimately turns out to be second best.

The class SearchProblem is used to store parameters and methods

needed to compute optimal actions.

class SearchProblem:

"""

A class to store a given parameterization of the "offer distribution

unknown" model.

"""

def __init__(self,

β=0.95, # Discount factor

c=0.3, # Unemployment compensation

F_a=1,

F_b=1,

G_a=3,

G_b=1.2,

w_max=1, # Maximum wage possible

w_grid_size=100,

π_grid_size=100,

mc_size=500):

self.β, self.c, self.w_max = β, c, w_max

self.f = jit(lambda x: p(x, F_a, F_b))

self.g = jit(lambda x: p(x, G_a, G_b))

self.π_min, self.π_max = 1e-3, 1-1e-3 # Avoids instability

self.w_grid = np.linspace(0, w_max, w_grid_size)

self.π_grid = np.linspace(self.π_min, self.π_max, π_grid_size)

self.mc_size = mc_size

self.w_f = np.random.beta(F_a, F_b, mc_size)

self.w_g = np.random.beta(G_a, G_b, mc_size)

The following function takes an instance of this class and returns

jitted versions of the Bellman operator T, and a get_greedy()

function to compute the approximate optimal policy from a guess v of

the value function

def operator_factory(sp, parallel_flag=True):

f, g = sp.f, sp.g

w_f, w_g = sp.w_f, sp.w_g

β, c = sp.β, sp.c

mc_size = sp.mc_size

w_grid, π_grid = sp.w_grid, sp.π_grid

@jit

def v_func(x, y, v):

return mlinterp((w_grid, π_grid), v, (x, y))

@jit

def κ(w, π):

"""

Updates π using Bayes' rule and the current wage observation w.

"""

pf, pg = π * f(w), (1 - π) * g(w)

π_new = pf / (pf + pg)

return π_new

@jit(parallel=parallel_flag)

def T(v):

"""

The Bellman operator.

"""

v_new = np.empty_like(v)

for i in prange(len(w_grid)):

for j in prange(len(π_grid)):

w = w_grid[i]

π = π_grid[j]

v_1 = w / (1 - β)

integral_f, integral_g = 0, 0

for m in prange(mc_size):

integral_f += v_func(w_f[m], κ(w_f[m], π), v)

integral_g += v_func(w_g[m], κ(w_g[m], π), v)

integral = (π * integral_f + (1 - π) * integral_g) / mc_size

v_2 = c + β * integral

v_new[i, j] = max(v_1, v_2)

return v_new

@jit(parallel=parallel_flag)

def get_greedy(v):

""""

Compute optimal actions taking v as the value function.

"""

σ = np.empty_like(v)

for i in prange(len(w_grid)):

for j in prange(len(π_grid)):

w = w_grid[i]

π = π_grid[j]

v_1 = w / (1 - β)

integral_f, integral_g = 0, 0

for m in prange(mc_size):

integral_f += v_func(w_f[m], κ(w_f[m], π), v)

integral_g += v_func(w_g[m], κ(w_g[m], π), v)

integral = (π * integral_f + (1 - π) * integral_g) / mc_size

v_2 = c + β * integral

σ[i, j] = v_1 > v_2 # Evaluates to 1 or 0

return σ

return T, get_greedy

We will omit a detailed discussion of the code because there is a more efficient solution method that we will use later.

To solve the model we will use the following function that iterates using T to find a fixed point

def solve_model(sp,

use_parallel=True,

tol=1e-4,

max_iter=1000,

verbose=True,

print_skip=5):

"""

Solves for the value function

* sp is an instance of SearchProblem

"""

T, _ = operator_factory(sp, use_parallel)

# Set up loop

i = 0

error = tol + 1

m, n = len(sp.w_grid), len(sp.π_grid)

# Initialize v

v = np.zeros((m, n)) + sp.c / (1 - sp.β)

while i < max_iter and error > tol:

v_new = T(v)

error = np.max(np.abs(v - v_new))

i += 1

if verbose and i % print_skip == 0:

print(f"Error at iteration {i} is {error}.")

v = v_new

if error > tol:

print("Failed to converge!")

elif verbose:

print(f"\nConverged in {i} iterations.")

return v_new

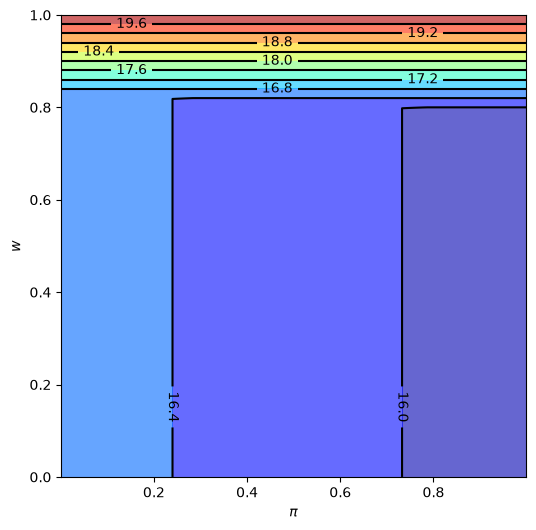

Let’s look at solutions computed from value function iteration

sp = SearchProblem()

v_star = solve_model(sp)

fig, ax = plt.subplots(figsize=(6, 6))

ax.contourf(sp.π_grid, sp.w_grid, v_star, 12, alpha=0.6, cmap=cm.jet)

cs = ax.contour(sp.π_grid, sp.w_grid, v_star, 12, colors="black")

ax.clabel(cs, inline=1, fontsize=10)

ax.set(xlabel=r'$\pi$', ylabel='$w$')

plt.show()

Error at iteration 5 is 0.6479122277746061.

Error at iteration 10 is 0.1032318911935981.

Error at iteration 15 is 0.022188780698234822.

Error at iteration 20 is 0.004884910305646528.

Error at iteration 25 is 0.0010812556698382991.

Error at iteration 30 is 0.00023934391512447917.

Converged in 33 iterations.

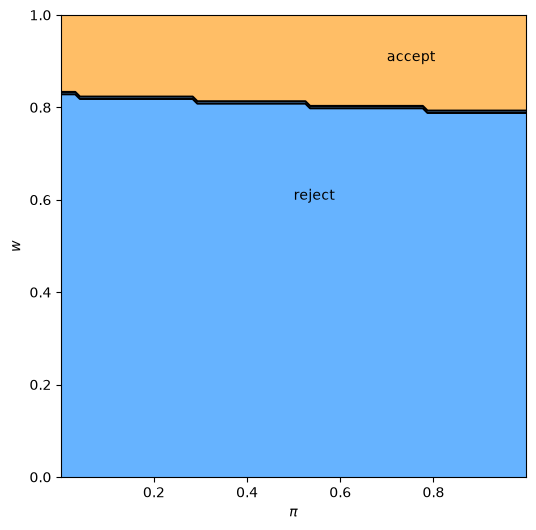

We will also plot the optimal policy

T, get_greedy = operator_factory(sp)

σ_star = get_greedy(v_star)

fig, ax = plt.subplots(figsize=(6, 6))

ax.contourf(sp.π_grid, sp.w_grid, σ_star, 1, alpha=0.6, cmap=cm.jet)

ax.contour(sp.π_grid, sp.w_grid, σ_star, 1, colors="black")

ax.set(xlabel=r'$\pi$', ylabel='$w$')

ax.text(0.5, 0.6, 'reject')

ax.text(0.7, 0.9, 'accept')

plt.show()

The results fit well with our intuition from section looking forward.

The black line in the figure above corresponds to the function \(\bar w(\pi)\) introduced there.

It is decreasing as expected.

57.4. Take 2: A More Efficient Method#

Let’s consider another method to solve for the optimal policy.

We will use iteration with an operator that has the same contraction rate as the Bellman operator, but

one dimensional rather than two dimensional

no maximization step

As a consequence, the algorithm is orders of magnitude faster than VFI.

This section illustrates the point that when it comes to programming, a bit of mathematical analysis goes a long way.

57.5. Another Functional Equation#

To begin, note that when \(w = \bar w(\pi)\), the worker is indifferent between accepting and rejecting.

Hence the two choices on the right-hand side of (57.3) have equal value:

Together, (57.3) and (57.4) give

Combining (57.4) and (57.5), we obtain

Multiplying by \(1 - \beta\), substituting in \(\pi' = \kappa(w', \pi)\) and using \(\circ\) for composition of functions yields

Equation (57.6) can be understood as a functional equation, where \(\bar w\) is the unknown function.

Let’s call it the reservation wage functional equation (RWFE).

The solution \(\bar w\) to the RWFE is the object that we wish to compute.

57.6. Solving the RWFE#

To solve the RWFE, we will first show that its solution is the fixed point of a contraction mapping.

To this end, let

\(b[0,1]\) be the bounded real-valued functions on \([0,1]\)

\(\| \omega \| := \sup_{x \in [0,1]} | \omega(x) |\)

Consider the operator \(Q\) mapping \(\omega \in b[0,1]\) into \(Q\omega \in b[0,1]\) via

Comparing (57.6) and (57.7), we see that the set of fixed points of \(Q\) exactly coincides with the set of solutions to the RWFE.

If \(Q \bar w = \bar w\) then \(\bar w\) solves (57.6) and vice versa.

Moreover, for any \(\omega, \omega' \in b[0,1]\), basic algebra and the triangle inequality for integrals tells us that

Working case by case, it is easy to check that for real numbers \(a, b, c\) we always have

Combining (57.8) and (57.9) yields

Taking the supremum over \(\pi\) now gives us

In other words, \(Q\) is a contraction of modulus \(\beta\) on the complete metric space \((b[0,1], \| \cdot \|)\).

Hence

A unique solution \(\bar w\) to the RWFE exists in \(b[0,1]\).

\(Q^k \omega \to \bar w\) uniformly as \(k \to \infty\), for any \(\omega \in b[0,1]\).

57.7. Implementation#

The following function takes an instance of SearchProblem and

returns the operator Q

def Q_factory(sp, parallel_flag=True):

f, g = sp.f, sp.g

w_f, w_g = sp.w_f, sp.w_g

β, c = sp.β, sp.c

mc_size = sp.mc_size

w_grid, π_grid = sp.w_grid, sp.π_grid

@jit

def ω_func(p, ω):

return np.interp(p, π_grid, ω)

@jit

def κ(w, π):

"""

Updates π using Bayes' rule and the current wage observation w.

"""

pf, pg = π * f(w), (1 - π) * g(w)

π_new = pf / (pf + pg)

return π_new

@jit(parallel=parallel_flag)

def Q(ω):

"""

Updates the reservation wage function guess ω via the operator

Q.

"""

ω_new = np.empty_like(ω)

for i in prange(len(π_grid)):

π = π_grid[i]

integral_f, integral_g = 0, 0

for m in prange(mc_size):

integral_f += max(w_f[m], ω_func(κ(w_f[m], π), ω))

integral_g += max(w_g[m], ω_func(κ(w_g[m], π), ω))

integral = (π * integral_f + (1 - π) * integral_g) / mc_size

ω_new[i] = (1 - β) * c + β * integral

return ω_new

return Q

In the next exercise, you are asked to compute an approximation to \(\bar w\).

57.8. Exercises#

Exercise 57.1

Use the default parameters and Q_factory to compute an optimal

policy.

Your result should coincide closely with the figure for the optimal policy shown above.

Try experimenting with different parameters, and confirm that the change in the optimal policy coincides with your intuition.

57.9. Solutions#

Solution

This code solves the “Offer Distribution Unknown” model by iterating on a guess of the reservation wage function.

You should find that the run time is shorter than that of the value function approach.

Similar to above, we set up a function to iterate with Q to find the

fixed point

def solve_wbar(sp,

use_parallel=True,

tol=1e-4,

max_iter=1000,

verbose=True,

print_skip=5):

Q = Q_factory(sp, use_parallel)

# Set up loop

i = 0

error = tol + 1

m, n = len(sp.w_grid), len(sp.π_grid)

# Initialize w

w = np.ones_like(sp.π_grid)

while i < max_iter and error > tol:

w_new = Q(w)

error = np.max(np.abs(w - w_new))

i += 1

if verbose and i % print_skip == 0:

print(f"Error at iteration {i} is {error}.")

w = w_new

if error > tol:

print("Failed to converge!")

elif verbose:

print(f"\nConverged in {i} iterations.")

return w_new

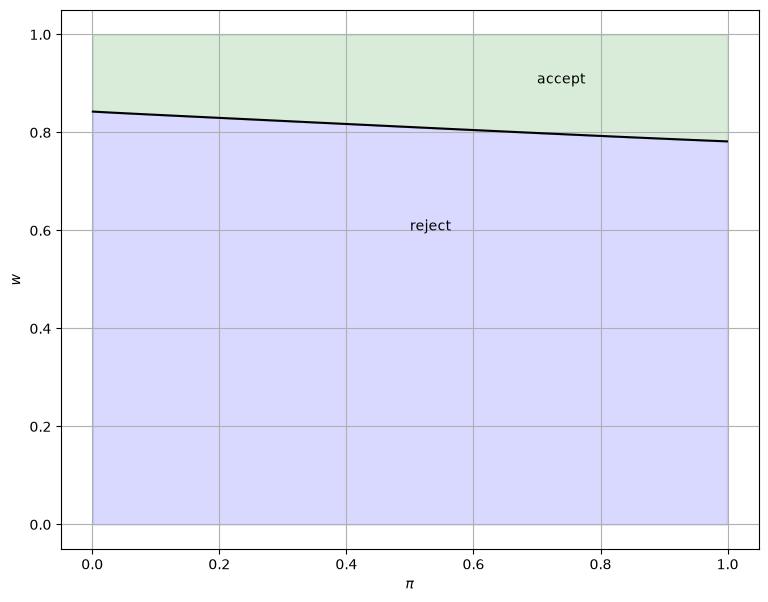

The solution can be plotted as follows

sp = SearchProblem()

w_bar = solve_wbar(sp)

fig, ax = plt.subplots(figsize=(9, 7))

ax.plot(sp.π_grid, w_bar, color='k')

ax.fill_between(sp.π_grid, 0, w_bar, color='blue', alpha=0.15)

ax.fill_between(sp.π_grid, w_bar, sp.w_max, color='green', alpha=0.15)

ax.text(0.5, 0.6, 'reject')

ax.text(0.7, 0.9, 'accept')

ax.set(xlabel=r'$\pi$', ylabel='$w$')

ax.grid()

plt.show()

Error at iteration 5 is 0.021835231479283235.

Error at iteration 10 is 0.006118427747488386.

Error at iteration 15 is 0.0012482653943254318.

Error at iteration 20 is 0.00024126252683831506.

Converged in 23 iterations.

57.10. Appendix A#

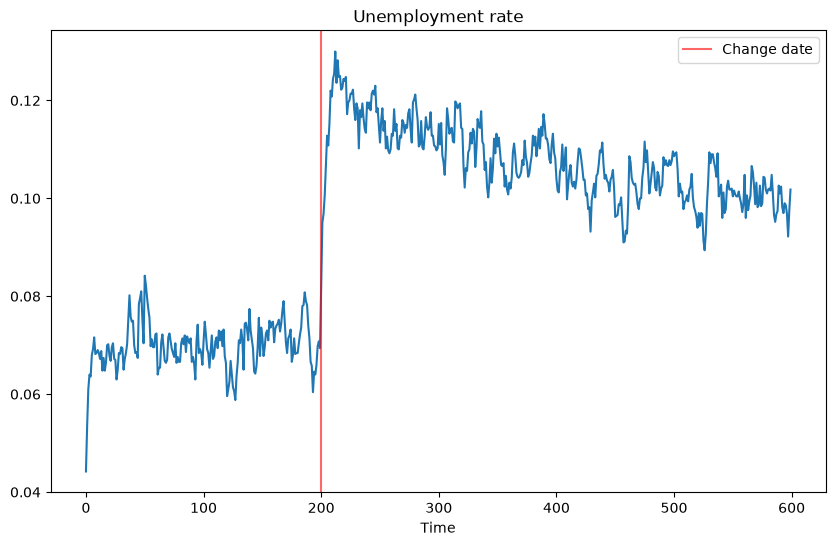

The next piece of code generates a fun simulation to see what the effect of a change in the underlying distribution on the unemployment rate is.

At a point in the simulation, the distribution becomes significantly worse.

It takes a while for agents to learn this, and in the meantime, they are too optimistic and turn down too many jobs.

As a result, the unemployment rate spikes

F_a, F_b, G_a, G_b = 1, 1, 3, 1.2

sp = SearchProblem(F_a=F_a, F_b=F_b, G_a=G_a, G_b=G_b)

f, g = sp.f, sp.g

# Solve for reservation wage

w_bar = solve_wbar(sp, verbose=False)

# Interpolate reservation wage function

π_grid = sp.π_grid

w_func = jit(lambda x: np.interp(x, π_grid, w_bar))

@jit

def update(a, b, e, π):

"Update e and π by drawing wage offer from beta distribution with parameters a and b"

if e == False:

w = np.random.beta(a, b) # Draw random wage

if w >= w_func(π):

e = True # Take new job

else:

π = 1 / (1 + ((1 - π) * g(w)) / (π * f(w)))

return e, π

@jit

def simulate_path(F_a=F_a,

F_b=F_b,

G_a=G_a,

G_b=G_b,

N=5000, # Number of agents

T=600, # Simulation length

d=200, # Change date

s=0.025): # Separation rate

"""Simulates path of employment for N number of works over T periods"""

e = np.ones((N, T+1))

π = np.full((N, T+1), 1e-3)

a, b = G_a, G_b # Initial distribution parameters

for t in range(T+1):

if t == d:

a, b = F_a, F_b # Change distribution parameters

# Update each agent

for n in range(N):

if e[n, t] == 1: # If agent is currently employment

p = np.random.uniform(0, 1)

if p <= s: # Randomly separate with probability s

e[n, t] = 0

new_e, new_π = update(a, b, e[n, t], π[n, t])

e[n, t+1] = new_e

π[n, t+1] = new_π

return e[:, 1:]

d = 200 # Change distribution at time d

unemployment_rate = 1 - simulate_path(d=d).mean(axis=0)

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(unemployment_rate)

ax.axvline(d, color='r', alpha=0.6, label='Change date')

ax.set_xlabel('Time')

ax.set_title('Unemployment rate')

ax.legend()

plt.show()

57.11. Appendix B#

In this appendix we provide more details about how Bayes’ Law contributes to the workings of the model.

We present some graphs that bring out additional insights about how learning works.

We build on graphs proposed in this lecture.

In particular, we’ll add actions of our searching worker to a key graph presented in that lecture.

To begin, we first define two functions for computing the empirical distributions of unemployment duration and π at the time of employment.

@jit

def empirical_dist(F_a, F_b, G_a, G_b, w_bar, π_grid,

N=10000, T=600):

"""

Simulates population for computing empirical cumulative

distribution of unemployment duration and π at time when

the worker accepts the wage offer. For each job searching

problem, we simulate for two cases that either f or g is

the true offer distribution.

Parameters

----------

F_a, F_b, G_a, G_b : parameters of beta distributions F and G.

w_bar : the reservation wage

π_grid : grid points of π, for interpolation

N : number of workers for simulation, optional

T : maximum of time periods for simulation, optional

Returns

-------

accpet_t : 2 by N ndarray. the empirical distribution of

unemployment duration when f or g generates offers.

accept_π : 2 by N ndarray. the empirical distribution of

π at the time of employment when f or g generates offers.

"""

accept_t = np.empty((2, N))

accept_π = np.empty((2, N))

# f or g generates offers

for i, (a, b) in enumerate([(F_a, F_b), (G_a, G_b)]):

# update each agent

for n in range(N):

# initial priori

π = 0.5

for t in range(T+1):

# Draw random wage

w = np.random.beta(a, b)

lw = p(w, F_a, F_b) / p(w, G_a, G_b)

π = π * lw / (π * lw + 1 - π)

# move to next agent if accepts

if w >= np.interp(π, π_grid, w_bar):

break

# record the unemployment duration

# and π at the time of acceptance

accept_t[i, n] = t

accept_π[i, n] = π

return accept_t, accept_π

def cumfreq_x(res):

"""

A helper function for calculating the x grids of

the cumulative frequency histogram.

"""

cumcount = res.cumcount

lowerlimit, binsize = res.lowerlimit, res.binsize

x = lowerlimit + np.linspace(0, binsize*cumcount.size, cumcount.size)

return x

Now we define a wrapper function for analyzing job search models with learning under different parameterizations.

The wrapper takes parameters of beta distributions and unemployment compensation as inputs and then displays various things we want to know to interpret the solution of our search model.

In addition, it computes empirical cumulative distributions of two key objects.

def job_search_example(F_a=1, F_b=1, G_a=3, G_b=1.2, c=0.3):

"""

Given the parameters that specify F and G distributions,

calculate and display the rejection and acceptance area,

the evolution of belief π, and the probability of accepting

an offer at different π level, and simulate and calculate

the empirical cumulative distribution of the duration of

unemployment and π at the time the worker accepts the offer.

"""

# construct a search problem

sp = SearchProblem(F_a=F_a, F_b=F_b, G_a=G_a, G_b=G_b, c=c)

f, g = sp.f, sp.g

π_grid = sp.π_grid

# Solve for reservation wage

w_bar = solve_wbar(sp, verbose=False)

# l(w) = f(w) / g(w)

l = lambda w: f(w) / g(w)

# objective function for solving l(w) = 1

obj = lambda w: l(w) - 1.

# the mode of beta distribution

# use this to divide w into two intervals for root finding

G_mode = (G_a - 1) / (G_a + G_b - 2)

roots = np.empty(2)

roots[0] = op.root_scalar(obj, bracket=[1e-10, G_mode]).root

roots[1] = op.root_scalar(obj, bracket=[G_mode, 1-1e-10]).root

fig, axs = plt.subplots(2, 2, figsize=(12, 9))

# part 1: display the details of the model settings and some results

w_grid = np.linspace(1e-12, 1-1e-12, 100)

axs[0, 0].plot(l(w_grid), w_grid, label='$l$', lw=2)

axs[0, 0].vlines(1., 0., 1., linestyle="--")

axs[0, 0].hlines(roots, 0., 2., linestyle="--")

axs[0, 0].set_xlim([0., 2.])

axs[0, 0].legend(loc=4)

axs[0, 0].set(xlabel='$l(w)=f(w)/g(w)$', ylabel='$w$')

axs[0, 1].plot(sp.π_grid, w_bar, color='k')

axs[0, 1].fill_between(sp.π_grid, 0, w_bar, color='blue', alpha=0.15)

axs[0, 1].fill_between(sp.π_grid, w_bar, sp.w_max, color='green', alpha=0.15)

axs[0, 1].text(0.5, 0.6, 'reject')

axs[0, 1].text(0.7, 0.9, 'accept')

W = np.arange(0.01, 0.99, 0.08)

Π = np.arange(0.01, 0.99, 0.08)

ΔW = np.zeros((len(W), len(Π)))

ΔΠ = np.empty((len(W), len(Π)))

for i, w in enumerate(W):

for j, π in enumerate(Π):

lw = l(w)

ΔΠ[i, j] = π * (lw / (π * lw + 1 - π) - 1)

q = axs[0, 1].quiver(Π, W, ΔΠ, ΔW, scale=2, color='r', alpha=0.8)

axs[0, 1].hlines(roots, 0., 1., linestyle="--")

axs[0, 1].set(xlabel=r'$\pi$', ylabel='$w$')

axs[0, 1].grid()

axs[1, 0].plot(f(x_grid), x_grid, label='$f$', lw=2)

axs[1, 0].plot(g(x_grid), x_grid, label='$g$', lw=2)

axs[1, 0].vlines(1., 0., 1., linestyle="--")

axs[1, 0].hlines(roots, 0., 2., linestyle="--")

axs[1, 0].legend(loc=4)

axs[1, 0].set(xlabel='$f(w), g(w)$', ylabel='$w$')

axs[1, 1].plot(sp.π_grid, 1 - beta.cdf(w_bar, F_a, F_b), label='$f$')

axs[1, 1].plot(sp.π_grid, 1 - beta.cdf(w_bar, G_a, G_b), label='$g$')

axs[1, 1].set_ylim([0., 1.])

axs[1, 1].grid()

axs[1, 1].legend(loc=4)

axs[1, 1].set(xlabel=r'$\pi$', ylabel=r'$\mathbb{P}\{w > \overline{w} (\pi)\}$')

plt.show()

# part 2: simulate empirical cumulative distribution

accept_t, accept_π = empirical_dist(F_a, F_b, G_a, G_b, w_bar, π_grid)

N = accept_t.shape[1]

cfq_t_F = cumfreq(accept_t[0, :], numbins=100)

cfq_π_F = cumfreq(accept_π[0, :], numbins=100)

cfq_t_G = cumfreq(accept_t[1, :], numbins=100)

cfq_π_G = cumfreq(accept_π[1, :], numbins=100)

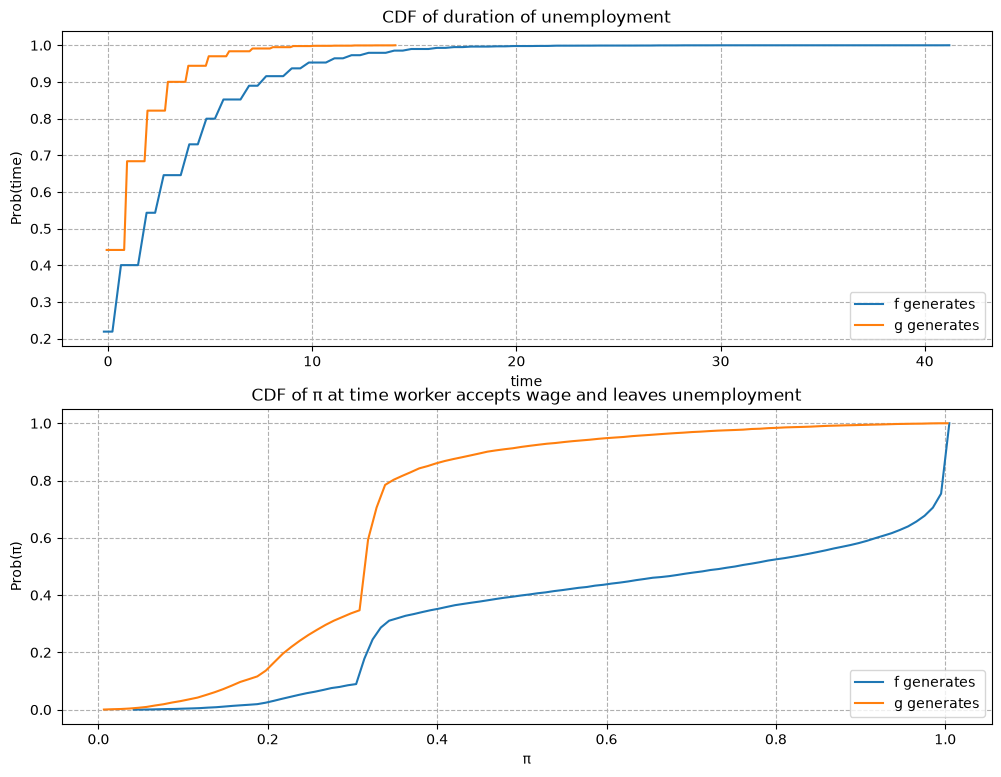

fig, axs = plt.subplots(2, 1, figsize=(12, 9))

axs[0].plot(cumfreq_x(cfq_t_F), cfq_t_F.cumcount/N, label="f generates")

axs[0].plot(cumfreq_x(cfq_t_G), cfq_t_G.cumcount/N, label="g generates")

axs[0].grid(linestyle='--')

axs[0].legend(loc=4)

axs[0].title.set_text('CDF of duration of unemployment')

axs[0].set(xlabel='time', ylabel='Prob(time)')

axs[1].plot(cumfreq_x(cfq_π_F), cfq_π_F.cumcount/N, label="f generates")

axs[1].plot(cumfreq_x(cfq_π_G), cfq_π_G.cumcount/N, label="g generates")

axs[1].grid(linestyle='--')

axs[1].legend(loc=4)

axs[1].title.set_text('CDF of π at time worker accepts wage and leaves unemployment')

axs[1].set(xlabel='π', ylabel='Prob(π)')

plt.show()

We now provide some examples that provide insights about how the model works.

57.12. Examples#

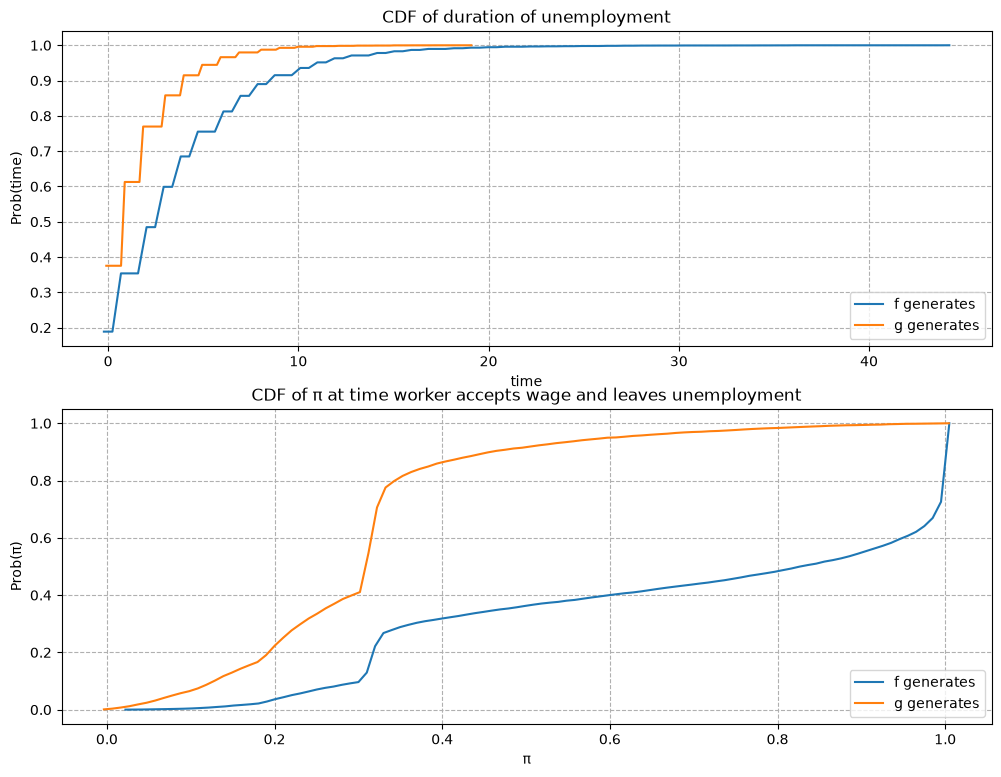

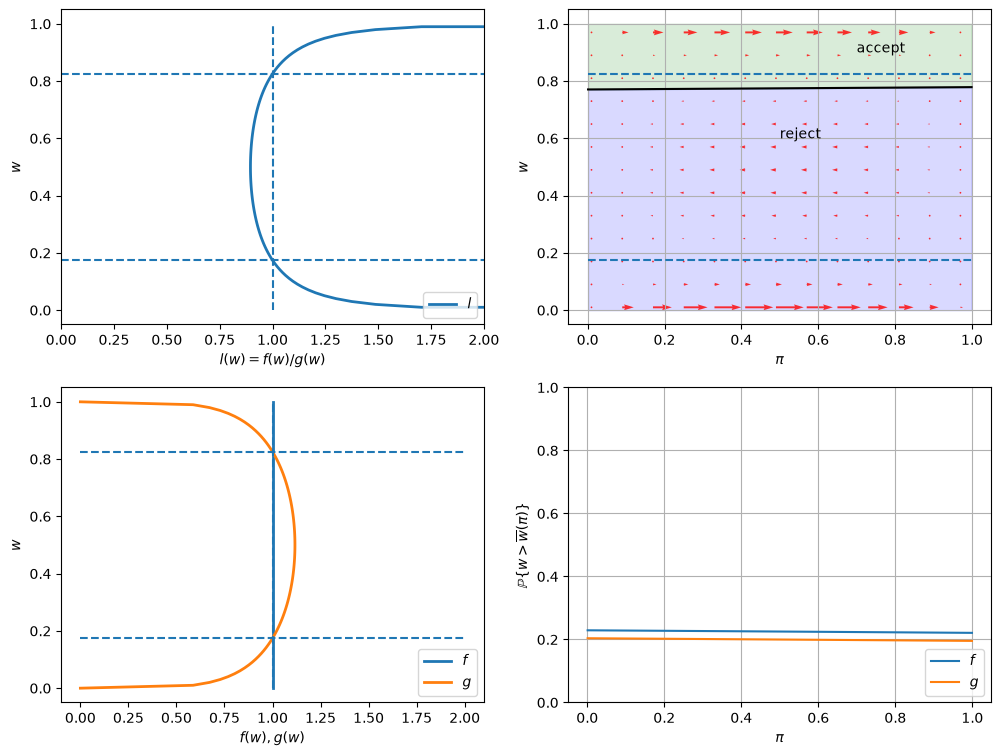

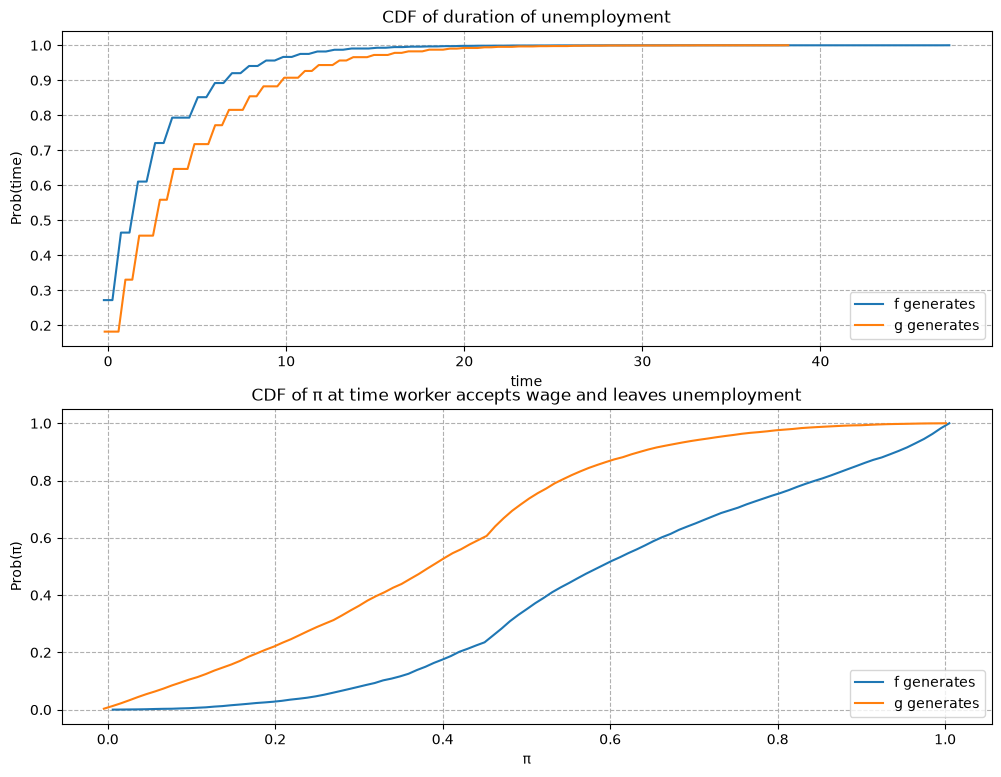

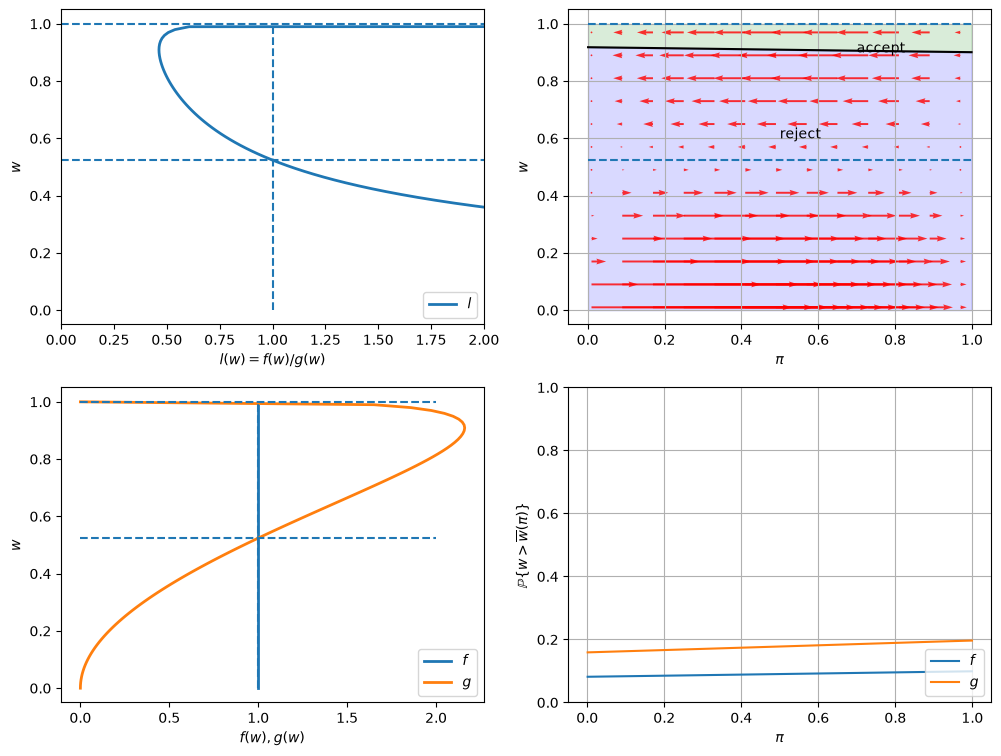

57.12.1. Example 1 (Baseline)#

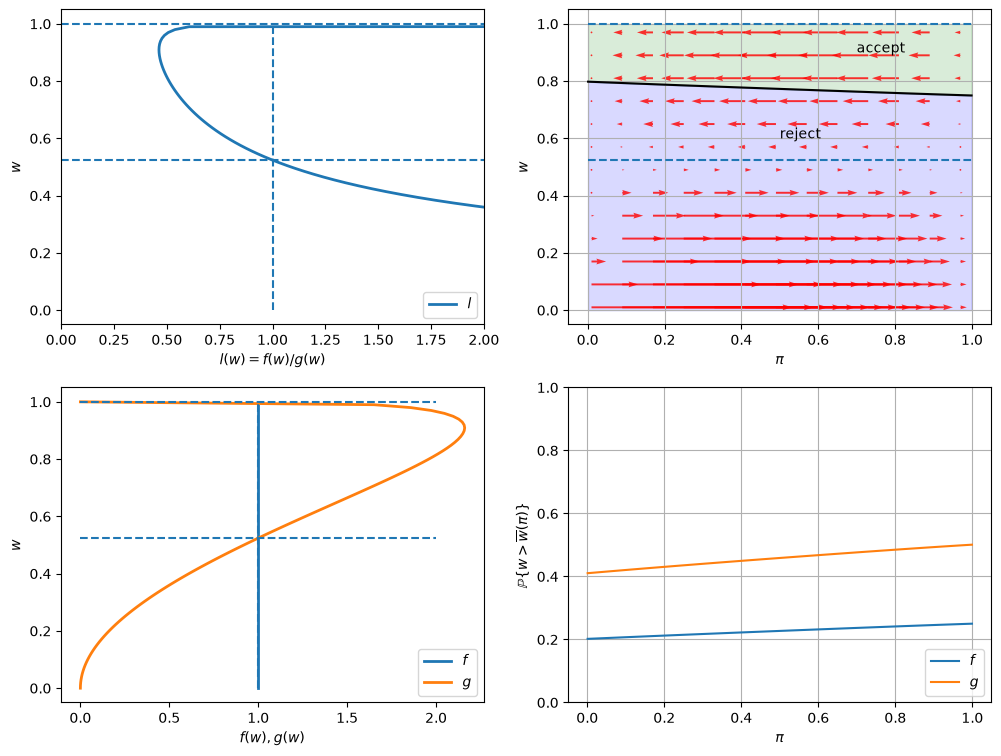

\(F\) ~ Beta(1, 1), \(G\) ~ Beta(3, 1.2), \(c\)=0.3.

In the graphs below, the red arrows in the upper right figure show how \(\pi_t\) is updated in response to the new information \(w_t\).

Recall the following formula from this lecture

The formula implies that the direction of motion of \(\pi_t\) is determined by the relationship between \(l(w_t)\) and \(1\).

The magnitude is small if

\(l(w)\) is close to \(1\), which means the new \(w\) is not very informative for distinguishing two distributions,

\(\pi_{t-1}\) is close to either \(0\) or \(1\), which means the priori is strong.

Will an unemployed worker accept an offer earlier or not, when the actual ruling distribution is \(g\) instead of \(f\)?

Two countervailing effects are at work.

if \(f\) generates successive wage offers, then \(w\) is more likely to be low, but \(\pi\) is moving up toward to 1, which lowers the reservation wage, i.e., the worker becomes less selective the longer he or she remains unemployed.

if \(g\) generates wage offers, then \(w\) is more likely to be high, but \(\pi\) is moving downward toward 0, increasing the reservation wage, i.e., the worker becomes more selective the longer he or she remains unemployed.

Quantitatively, the lower right figure sheds light on which effect dominates in this example.

It shows the probability that a previously unemployed worker accepts an offer at different values of \(\pi\) when \(f\) or \(g\) generates wage offers.

That graph shows that for the particular \(f\) and \(g\) in this example, the worker is always more likely to accept an offer when \(f\) generates the data even when \(\pi\) is close to zero so that the worker believes the true distribution is \(g\) and therefore is relatively more selective.

The empirical cumulative distribution of the duration of unemployment verifies our conjecture.

job_search_example()

57.12.2. Example 2#

\(F\) ~ Beta(1, 1), \(G\) ~ Beta(1.2, 1.2), \(c\)=0.3.

Now \(G\) has the same mean as \(F\) with a smaller variance.

Since the unemployment compensation \(c\) serves as a lower bound for bad wage offers, \(G\) is now an “inferior” distribution to \(F\).

Consequently, we observe that the optimal policy \(\overline{w}(\pi)\) is increasing in \(\pi\).

job_search_example(1, 1, 1.2, 1.2, 0.3)

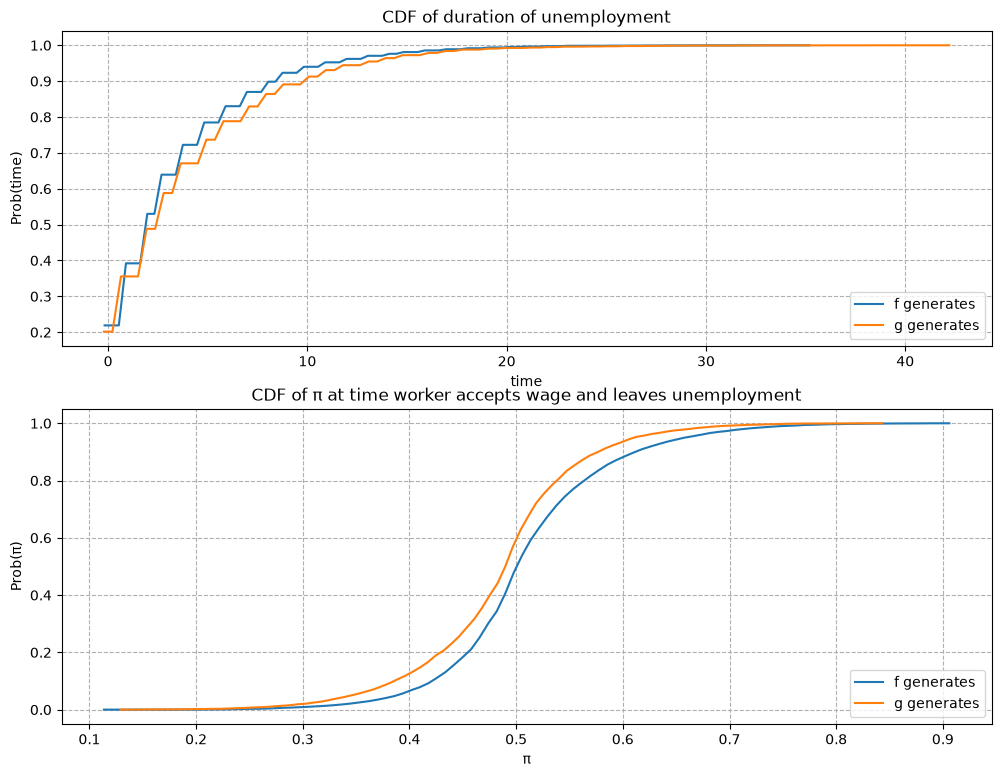

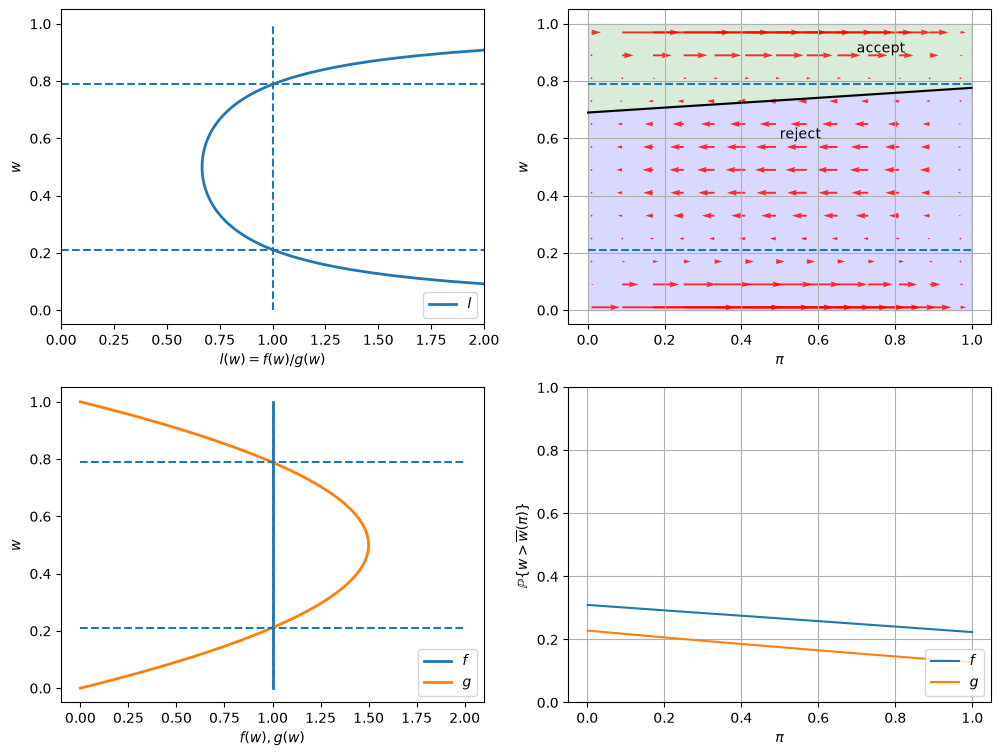

57.12.3. Example 3#

\(F\) ~ Beta(1, 1), \(G\) ~ Beta(2, 2), \(c\)=0.3.

If the variance of \(G\) is smaller, we observe in the result that \(G\) is even more “inferior” and the slope of \(\overline{w}(\pi)\) is larger.

job_search_example(1, 1, 2, 2, 0.3)

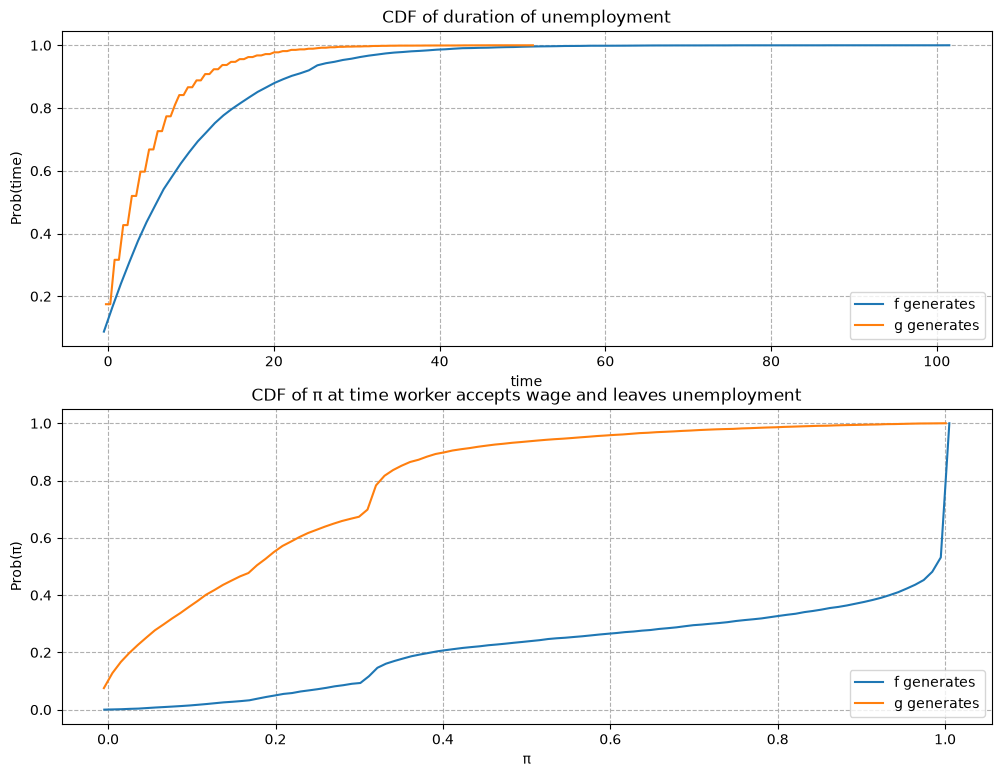

57.12.4. Example 4#

\(F\) ~ Beta(1, 1), \(G\) ~ Beta(3, 1.2), and \(c\)=0.8.

In this example, we keep the parameters of beta distributions to be the same with the baseline case but increase the unemployment compensation \(c\).

Comparing outcomes to the baseline case (example 1) in which unemployment compensation if low (\(c\)=0.3), now the worker can afford a longer learning period.

As a result, the worker tends to accept wage offers much later.

Furthermore, at the time of accepting employment, the belief \(\pi\) is closer to either \(0\) or \(1\).

That means that the worker has a better idea about what the true distribution is when he eventually chooses to accept a wage offer.

job_search_example(1, 1, 3, 1.2, c=0.8)

57.12.5. Example 5#

\(F\) ~ Beta(1, 1), \(G\) ~ Beta(3, 1.2), and \(c\)=0.1.

As expected, a smaller \(c\) makes an unemployed worker accept wage offers earlier after having acquired less information about the wage distribution.

job_search_example(1, 1, 3, 1.2, c=0.1)